The Confident Chronicles: June 11, 2026

INVESTOR UPDATE:

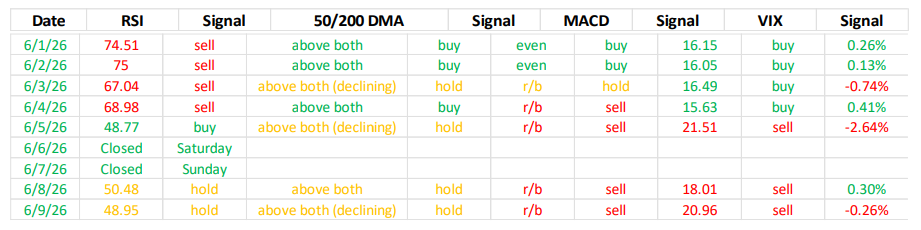

The technical indicators we monitor for the Tactical models have had 3 days with two (or more) in the “risk off” position. (See Chart Below)

As of today, the Tactical Models will move half the equity positions to cash due to the changes in the technical indicators we follow

The “MACD” (Moving Average Convergence/Divergence) measures momentum and changed from a “buy” signal on June 3 rd. The VIX (Volatility Index) measures the amount of “fear” in the market and turned negative on June 5th.

The S&P 500 is about to breach its 50 day moving average which will put the market on notice. If the S&P cannot rise above the “50 day” in a short amount of time, we may be in for a prolonged sell off.

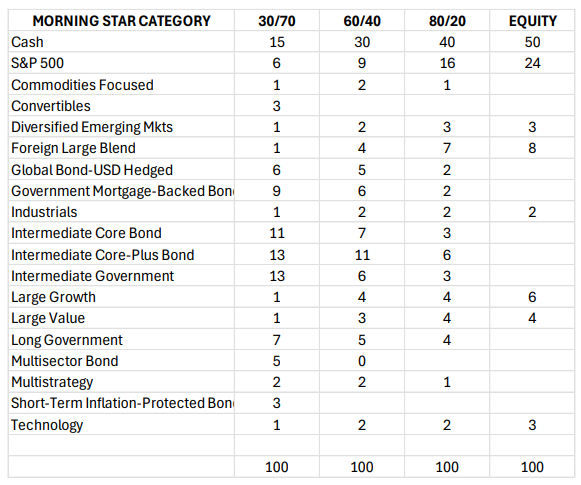

CURRENT ALLOCATIONS - TACTICAL MODELS:

Current Allocations are the monies currently in your plan.

Making changes to this money is known as a “rebalance”.

Some plans have trading restrictions on how often you can rebalance the money in your plan. Be sure to know your plan’s restrictions before implementing any tactical strategies.

Our “Tactical Models” combine the benefits of asset allocation and “momentum investing” strategies. These models rebalance periodically back to their risk “targets” and the targets can be changed at any time given the current market conditions.

These models may go through periods of time while holding larger amounts of cash than the Strategic Models.

Our Tactical Models may rebalance on any given day.

Please be sure to look for an email from support@planconfidence.com letting you know when to make changes.

Tactical Models UPDATED Today 06/11/2026

See below for the asset allocation for each model.

The exact amounts you should allocate depend on the model that you are using and the options available in your plan. These categories may or may not be available in your plan.

If they are not available in your plan, we will recommend the closest available asset class and label it as a “proxy”.

You can find all substitutions on your “Proxy Page” within your dashboard.

Please log into your Participant Dashboard to see the exact allocations you should be using as of the last rebalance advice.

Please talk to your adviser if you have any questions.

BLACKROCK MODEL UPDATE:

Trade Rationale:

It seems we have been early to many of today’s most fashionable portfolio themes, and that positioning has been rewarded as markets moved sharply higher from earlier-year lows – and now flirt with fresh all-time highs. The important nuance is that many of the same risks that rattled investors a few months ago still largely exist today; the difference is that markets are now confronting them from a much higher starting point. We aren't calling a market peak, but the incremental payoff from maintaining a chunky broad equity overweight has admittedly cooled at the margin.

Crucially, the macro backdrop still looks constructive in our view. Earnings have been exceptionally strong, the U.S. has remained better insulated than much of the world from elevated energy prices, and the technology and AI buildout has continued to support a meaningful productivity impulse. Inflation has pushed higher in the short run, but much of that appears tied to visible and likely nonstructural drivers. Namely, oil and energy pressures linked to Middle East tensions and related supply disruptions, rather than a narrative breaking reacceleration in underlying inflation. Strip out some of that noise, and there is still a reasonable case that broader inflation pressures could ease over time.

That said, the path is messy. Kevin Warsh has taken the helm as Fed Chair and brings a new, supply-side perspective to the table. Warsh has openly recognized that the AI-driven productivity boom requires vast capital capacity, meaning the Fed could have a legitimate justification to cut interest rates later this year; not because the economy is weak, but to ensure that lending and investing don't become unnecessarily burdensome to an industrial revolution. Warsh has even hinted at moving the inflation goalposts, shifting the Fed's focus from core Personal Consumption Expenditures (PCE)to a trimmed-mean version of inflation to potentially better isolate true underlying economic signals from temporary energy spikes. While this structural shift may be a long-term positive, the transition itself has introduced real policy uncertainty. Jerome Powell’s decision to remain on the Board of Governors introduces a hawkish dual-leadership dynamic that inevitably clouds how incoming data will be interpreted. Because of this institutional friction, the absolute probability of rate cuts is undoubtedly lower than it was at the start of the year.

These yellow flags are why we’re being more intentional about where our risk lives. In the areas where our conviction is highest, such as AI and innovation, U.S. over international developed markets, and growth over value, we have continued to run well off benchmark. Where conviction is lower, we’re aiming to harvest that active risk and reallocate it either more efficiently (low-cost market exposure) or more effectively (active strategies). This includes an actively managed country selection strategy for our international exposure that we run in-house based on our own proprietary investment signals. In the same vein, we’re carving out space for a bond-funded liquid alternatives position, a nimble, regime-based engine that hunts for excess returns and provides genuine, uncorrelated sources of diversification, which is especially attractive when traditional fixed income struggles to provide real ballast.

In short, this trade is less “hero call” fade of a red-hot rally and more an effort of prudent portfolio management. We maintain a core anchor toward the secular drivers of this market cycle, while quietly recognizing that locking in some gains and redeploying risk into potentially more efficient, precise expressions may be a smarter move today than it was when markets were lower and fear was louder.

This information should not be relied upon as investment advice, research, or a recommendation by BlackRock regarding (i) the funds, (ii) the use or suitability of the model portfolios or (iii) any security in particular. Only an investor and their financial professional know enough about their circumstances to make an investment decision.

This update has been written by Kevin T Clark, RF™.

All opinions expressed are those of the author and not that of Plan Confidence Corporation nor any other firm or individual.

Kevin T Clark, RF™ is the CEO and Co-founder of Plan Confidence Corporation. Kevin is an “ERISA Nerd” and one of only a hundred(ish) Dalbar certified Registered Fiduciaries (RF™) in the United States.

He has been helping hard working Americans invest their money since 1997!

Plan Confidence Corporation is an SEC registered “internet only” investment firm specializing in providing advice to hard-working Americans investing in their employer’s retirement plans (401k, 403b, TSP, etc).

They have created proprietary software so hard-working Americans can receive professional, ongoing advice on their employer’s retirement plan from an adviser of their choosing!

PlanConfidence believes that EVERY 401(k) participant should be getting professional, ongoing advice from an adviser of their choosing!

#401kAdvice #403bAdvice #TSPadvice #BeConfident #got401k